Executive Summary

- Special assessments avoid corporate interest costs but frequently cause severe financial hardship for individual unit owners facing immediate lump-sum demands.

- Condo corporation loans spread repair costs over time through manageable monthly common expense increases, protecting vulnerable residents.

- Hybrid funding models allow owners to choose between paying their portion as an upfront lump sum or joining the corporate loan.

- Condominium Lending Group (CLG) offers specialized condo corporation financing that does not require personal guarantees or individual unit liens.

The Funding Dilemma for Condo Boards

How do you fund critical infrastructure repairs without bankrupting your neighbors? If your corporation needs immediate capital, a condo corporation loan is often the financially responsible choice over a massive cash call. Many aging buildings face contingency fund shortfalls requiring rapid capital injection. This guide compares the financial mechanics of strata financing versus mandatory levies to help directors make equitable, legally compliant funding decisions.

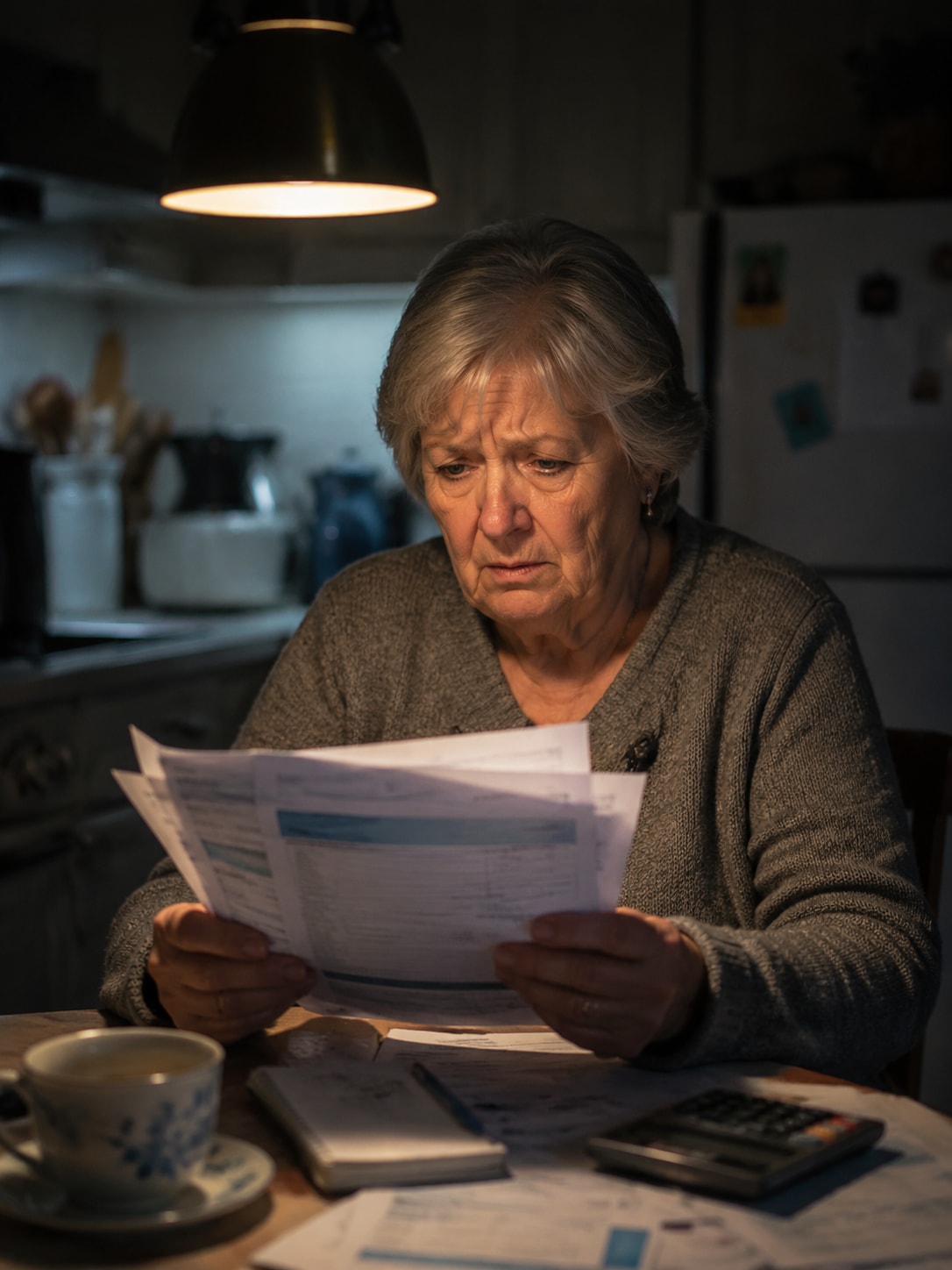

Capital reserve studies often reveal massive shortfalls at the worst possible time. A roof fails. A parking garage requires immediate structural retrofitting. Directors and property managers are then thrust into a highly stressful position. They must fulfill their fiduciary duty to maintain the property while managing the harsh financial reality of their ownership base. If your community is highly affluent, universally able to write large checks, and completely debt-averse, a lump-sum demand might work. For the vast majority of Canadian communities, demanding tens of thousands of dollars within 30 days is catastrophic.

This article strictly compares how to fund major repairs using corporate debt, hybrid models, and strategic planning. We will analyze the impact on unit holders, legal compliance requirements, and long-term equity to guide your strata council toward the most stable financial resolution. According to Special Assessment vs Condo Loan: When to Update Your Reserve Fund Study, mandatory charges force current residents to pay for improvements that future buyers will enjoy.

Corporate debt facilities excel at manageability. They convert massive upfront capital requirements into predictable monthly payments. Data from Special Assessment vs. Condo Corporation Loans: Which is Really Best for Your Condo Board? shows that while borrowing adds interest expenses to the operating budget, it prevents sudden financial hardship. This approach protects vulnerable residents from taking on high-interest personal debt.

Consider a major structural repair project across a large multi-unit building. A sudden cash call demands a significant unexpected payment from each shareholder, usually required within a short timeframe. This financial shock forces many to drain retirement savings, take out personal loans, or sell their units below market value in a distressed state. The council may avoid corporate interest, but the hidden cost is transferred directly to the residents’ personal balance sheets.

Strata corporation loans allow communities to spread the burden of large projects over a longer period. Instead of a massive lump sum, residents see a manageable monthly maintenance fee increase. If you are exploring Article Funding Condo Repairs Without Special Levies, it becomes clear that corporate financing smooths cash flow. Specialized lenders like CLG structure these facilities without requiring personal guarantees. They never place liens on individual units. The debt is secured against the corporation’s future common expense revenues, leaving individual mortgages entirely unaffected.

Intergenerational Equity: Who Pays for the Roof?

Debt financing ensures fairness. It aligns the cost of a capital asset with its useful life. According to Special Assessment vs Condo Loan: When to Update Your Reserve Fund Study, lump-sum demands force current residents to pay 100% of costs for improvements that future buyers will enjoy. Corporate borrowing ensures equitable distribution of these expenses over time.

The concept of intergenerational equity is central to responsible fiduciary management. If a strata corporation installs a new roof, a cash call forces the people living in the building today to pay for the entire lifespan of that asset. If someone sells their unit shortly after paying for a major repair, they have effectively subsidized the remaining lifespan of that improvement for the new buyer.

What is the difference between a strata debt facility and a mandatory cash call in this context? A loan matches the payment schedule to the asset’s lifespan. As people sell and move out, the new buyers take over the monthly common expense payments that service the debt. This ensures that whoever lives under the roof pays for the roof. We explore this dynamic further in The Role Of Loans In Supporting Condominium Communities, highlighting how financing prevents current residents from being unfairly penalized for historical underfunding.

Approval Process and Legal Compliance

Cash calls offer rapid execution. However, borrowing wins for community harmony. As discussed in Condominium Loans and Special Assessments with Jim Wallace, passing a borrowing bylaw requires more administrative effort. Yet, it builds essential transparency. This democratic process ensures unit holders understand and support the financial direction of the corporation.

Under most provincial Condominium Acts and the BC Strata Property Act, directors hold the authority to levy a mandatory charge without a vote if the funds are required for an emergency or to comply with a structural engineering mandate. This allows for rapid capital collection. Bypassing the ownership base, however, frequently results in immense backlash, hostile town halls, and even legal challenges against the fiduciaries.

Securing a debt facility involves a more rigorous approval process. Councils must pass a borrowing bylaw, which typically requires a majority vote from the community. Proponents of cash calls argue that voting delays critical repairs. The reality is that presenting a well-structured financing option usually results in overwhelming support. Qualification requirements generally include an updated reserve fund study, clean financial statements, and a demonstrated ability to service the monthly debt through common expense fees.

The Hybrid Approach: Opt-In/Opt-Out Funding

Is there a middle ground? Yes. The hybrid model provides an excellent compromise by allowing residents to choose between upfront payments and long-term financing. Based on insights from Special Assessments in Alberta Condos | Sticker Shock Explained, this opt-in/opt-out structure accommodates both cash-rich individuals and those on fixed incomes. It effectively neutralizes friction during major capital projects.

When evaluating hybrid options, the mechanics are straightforward. The directors pass a special levy for the total project cost while simultaneously securing a corporate credit facility for the exact same amount. Everyone receives a choice. Those who have the cash on hand can pay their portion upfront, entirely avoiding their share of the corporate interest costs.

Those who cannot afford the lump sum simply opt into the corporate facility. The corporation draws down only the exact amount of funds required to cover the participating units. The monthly debt service costs are then allocated specifically to those participating units. This is the most democratic solution available to modern fiduciaries, accommodating debt-averse individuals while protecting vulnerable neighbors from financial ruin.

Which Is Right for Your Corporation?

Selecting the correct funding mechanism depends on project scale, demographics, and urgency. While Condo Financing Myths Debunked notes that many councils fear corporate debt, strategic financing often proves safer than depleting personal savings. We recommend evaluating these factors objectively before drafting a borrowing bylaw.

Choose Special Assessments ONLY IF:

- The repair is generally considered minor.

- The ownership base is highly affluent and has indicated a preference for lump-sum payments.

- The timeline is extremely tight due to an immediate life-safety emergency where a standard voting period is impossible.

Choose a Condo Loan IF:

- The repair is structural or major.

- A significant portion of residents are on fixed incomes or would struggle to secure personal financing.

- The council wants to align the cost of the asset with its useful lifespan to ensure intergenerational equity.

Choose Hybrid Funding IF:

- The community is economically diverse.

- The directors want to minimize friction and offer maximum flexibility.

- You have the administrative capacity to track split payment streams.

Limitations & Alternatives

Deferring maintenance is never a viable alternative. Inflation consistently outpaces construction delays. One common mistake we see is councils ignoring structural repairs to avoid backlash, which ultimately increases legal liabilities and final costs. Acknowledging the limitations of both financing and mandatory levies is crucial for fiduciary responsibility.

While we advocate for corporate borrowing to protect communities, we must acknowledge the limitations. Debt facilities add interest expenses to the bottom line. Financing the project over a long term will result in a higher total cost than if it were funded in cash today. Carrying corporate debt can sometimes prompt questions from prospective buyers. A well-explained facility for a brand-new roof, however, is generally viewed more favorably than an underfunded reserve and a deteriorating building.

If directors are looking at how to fund major repairs without borrowing or cash calls, the only other alternative is phasing construction projects over several years. This allows the council to match expenses with incoming reserve contributions. This approach fails when dealing with critical building envelope failures or structural concrete decay, where delays pose severe safety risks. Reviewing resources like the Condo Corporation Loan FAQ can help fiduciaries understand exactly what limitations apply to their specific provincial jurisdiction.

Frequently Asked Questions

What is the difference between a condo loan and a special assessment?

A special assessment is a mandatory, lump-sum charge levied against unit owners to cover immediate corporate shortfalls, usually payable within 30 to 90 days. A condo loan is money borrowed by the corporation itself, which is paid back over time through a manageable increase in monthly common expense fees.

How common are special assessments in condos?

They are increasingly common across Canada due to historic underfunding of reserves and rapid construction inflation. Many aging buildings will face a capital shortfall requiring either a mandatory levy or corporate financing within the next decade.

Do condo loans require a lien on my individual unit?

No. Specialized corporate facilities, such as those provided by CLG, do not require individual unit liens or personal guarantees from residents or directors. The debt is secured entirely against the corporation’s future right to collect common expense fees.

Can a condo board borrow money without a special assessment?

Yes. Under most provincial legislation, a council can borrow money by passing a borrowing bylaw. This typically requires a majority vote from the community. Once passed, the directors secure the funds and increase monthly maintenance fees to cover the debt service, bypassing the need for a lump-sum demand.

What is the difference between condo loss assessment and special assessment?

A special assessment is a charge levied by the directors to pay for property repairs or shortfalls. Condo loss assessment coverage is a specific clause in an individual’s personal home insurance policy that may reimburse them if the corporation issues a levy resulting from a covered insurable peril (like fire or severe storm damage).

How long does it take to get approval for a strata loan?

The timeline for strata corporation financing typically takes several weeks to complete. The lender can usually provide a term sheet within a week. The bulk of the timeline is dictated by the statutory notice periods required to call a special general meeting and hold the vote for the borrowing bylaw.

Protect Your Community’s Financial Health

Lump-sum levies have historically been the default mechanism for addressing capital shortfalls. Today, modern fiduciaries increasingly recognize that corporate borrowing is often the more responsible choice. By converting massive upfront capital demands into predictable monthly payments, councils can fund critical infrastructure repairs equitably while protecting vulnerable neighbors from severe financial distress.

Ready to explore customized financing structures that do not require personal guarantees or unit liens? Reach out to our team of specialists via our Contact Us page to discuss your specific shortfall and find the right solution for your building.