This article is based on CLG’s Water Events: Prevention, Response and Financial Impact webinar featuring insights from NorGaard Solutions, Renolux Restore Group, LEaC Shield, and Condominium Lending Group, but it is written as a practical guide for condo boards and property managers dealing with deductibles, self-insured losses, and water damage repair costs.

Watch the full webinar here: Water Events: Prevention, Response and Financial Impact

Hosted by:

- Aaron Norgaard, NorGaard Solutions, water event prevention, pipe corrosion management, and leak detection systems

- Amanda Silvestri, Renolux Restore Group, emergency water event response, moisture control, and restoration

- Lyndsey McNally, Condominium Lending Group, condo corporation financial planning and financing

- Ruth Tompkins, LEaC Shield, water event risk management

Condo insurance deductible financing: how boards fund water damage costs without a special assessment

Water damage is one of the most common insurance problems in Canadian condominium buildings. TD Insurance Home data cited by the Insurance Bureau of Canada puts water damage at 40% of condo insurance claims. Most boards already know water is a recurring risk. The surprise comes later, when the corporation finds out what the insurer does not cover.

After a water event, three costs often land on the corporation’s balance sheet: the deductible, smaller losses below the deductible, and repairs to the failed system that caused the leak. Most reserve fund studies do not model those costs in a useful way. When they hit at the same time, the board has to find money quickly. A special assessment is the usual fallback. It is understandable, but it can also create serious friction with owners.

For some corporations, condo insurance deductible financing is another option. The corporation borrows to cover the gap, then repays the loan through monthly common expenses. That can give the board a more practical way to deal with a large deductible or uninsured repair cost without sending owners a sudden five-figure bill.

Main takeaways

- Water damage causes 40% of condo insurance claims in Canada, but the deductible, smaller self-insured losses, and repairs to the leak source can still fall on the corporation.

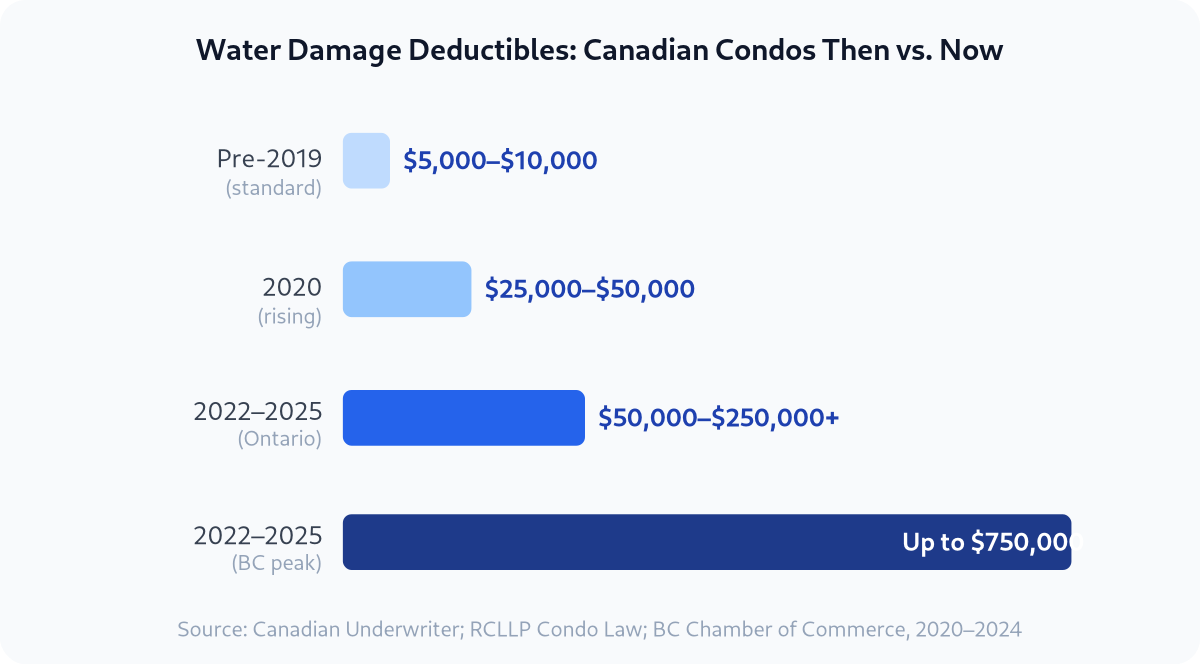

- Water damage deductibles for Ontario condo corporations have risen sharply since 2019. In some cases, they now fall in the $50,000 to $250,000 range, with higher numbers reported in parts of BC.

- Corporation borrowing can spread those costs through monthly common expenses instead of relying only on a lump-sum special assessment.

What water damage actually costs a condo corporation

In 2024, Canada’s insurers paid out $8.5 billion in severe weather losses, almost three times the $2.8 billion recorded in 2023, according to the Insurance Bureau of Canada. Water damage from plumbing failures is a major issue in multi-unit residential buildings. But the claim handled by the insurer is only part of what the corporation may have to pay.

Three cost categories are often outside standard property coverage.

1. The insurance deductible

The deductible is the corporation’s first-dollar responsibility on a claim. Before 2019, typical condo insurance deductibles in Canada often sat between $5,000 and $10,000. Those numbers are no longer a safe assumption. By 2024, water-damage-specific deductibles for Ontario condo corporations were often reported in the $50,000 to $250,000 range, with some BC stratas facing per-occurrence deductibles as high as $750,000 on water claims.

That deductible is usually due right away. It is not paid in installments. If the reserve fund or operating fund cannot absorb it, the board needs another funding source.

2. Self-insured losses below the deductible

Boards tend to focus on the large deductible, but smaller events can add up quickly. If the corporation has a $100,000 deductible, a $20,000 bathroom flood or a $35,000 hallway repair is paid entirely by the corporation. Insurance pays nothing because the loss sits below the deductible.

Those self-insured losses rarely show up cleanly in a reserve fund study. Reserve studies model scheduled replacements. They do not usually plan for a run of smaller water events caused by aging plumbing, failed appliances, or hidden moisture.

The cost of a small water event can surprise even experienced people. While preparing for the webinar behind this article, Lyndsey McNally had a water loss in her own home. It was clean water from a hose. Amanda Silvestri’s team at Renolux Restore Group led the response. What looked minor turned into $30,000 in damage, much of it hidden behind walls and under floors. Lyndsey would not have identified the full extent of it without professional moisture mapping equipment.

The point is not drama. It is math. Self-insured events can cost more than they look, and if the wrong vendor misses moisture behind walls or under finishes, the final bill can climb.

3. Repairing the cause of the leak

This is the part many boards do not expect. Property insurance may cover the resulting damage, such as damaged drywall, flooring, cabinets, and finishes. It does not usually cover the cause of the loss. If a plumbing riser fails and floods four suites, the insurer may restore the suites. Replacing the failed riser section is the corporation’s bill.

In 2024, complete plumbing riser replacement projects in Toronto-area condo buildings were often estimated between $500,000 and $2,000,000, according to Hudson HVAC, a Toronto-based riser replacement specialist. That is not a small operating expense.

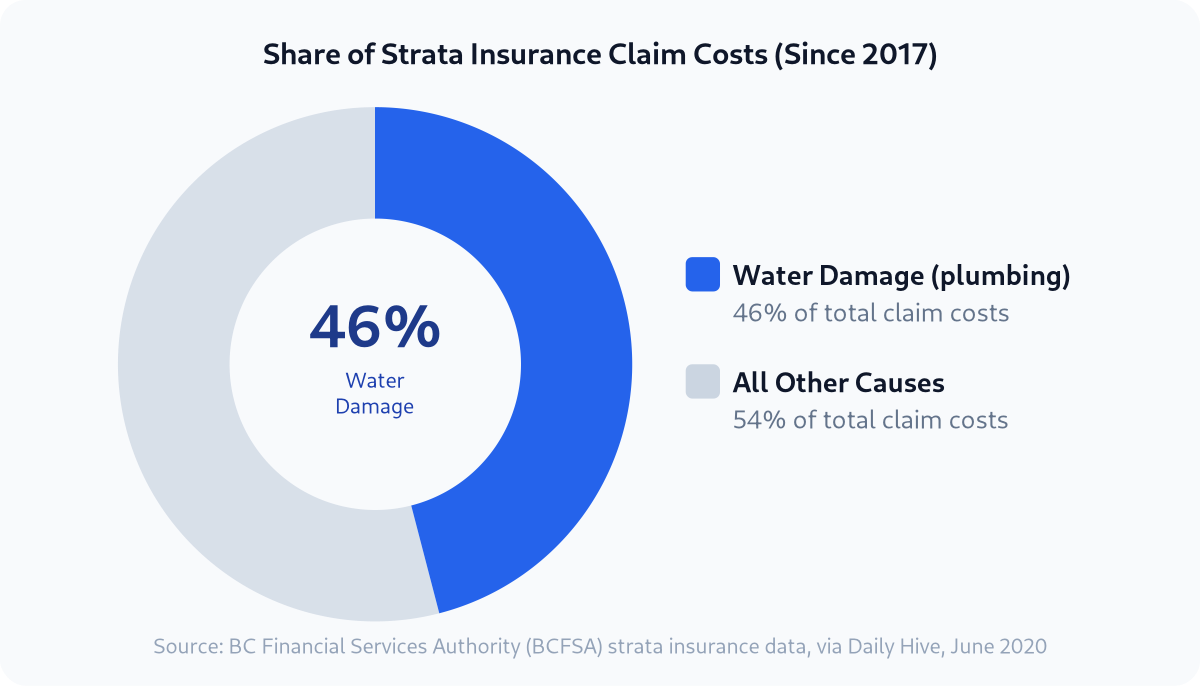

BC Financial Services Authority data cited in reporting on strata insurance found that water damage accounted for 46% of total strata insurance claim costs since 2017. That figure reflects what insurers handled. It does not capture every deductible, every below-deductible loss, or every repair to the system that caused the problem.

Reserve fund shortfalls created by water events have a financing path. See CLG’s reserve fund and financial planning solutions for how boards address those gaps.

As of 2024, water damage deductibles for Ontario condo corporations can reach $250,000, up from much lower pre-2019 levels reported by Canadian Underwriter and RCLLP Condo Law. The deductible, smaller self-insured losses, and uninsured repairs can all hit at once.

Why older condo buildings face more water damage exposure

Plumbing risers corrode. That is not a scare line. It is how metal plumbing ages. In many concrete frame buildings, corrosion becomes a serious operating problem around the 30-year mark. Buildings from the 1980s and 1990s are now in that window.

At CLG’s Water Events: Prevention, Response and Financial Impact webinar, Aaron Norgaard of NorGaard Solutions shared a case that makes the financial issue easy to understand. A building averaging one pinhole leak per month was facing a projected $1.5 million plumbing riser replacement. Instead, the board invested in a LEaC Shield sodium silicate dosing system, which forms a ceramic coating inside the pipes to seal pinhole leaks and slow further corrosion. The result was a 99% reduction in leaks, and the full replacement cost was avoided.

Another webinar example came from Vancouver. The building had so many major water events that it was close to becoming uninsurable. Its deductible had reached $250,000, annual premiums had increased by $90,000, and each resident had to carry an individual policy of about $1,000 per year. After the building installed a Safe House LoRa-based sensor network with automatic shutoffs, the deductible dropped to $75,000, premiums fell by $80,000, and residents no longer had to carry that separate coverage.

CLG is not a prevention company. We do not sell sensors, pipe treatments, or restoration services. These examples matter because they show how deferred maintenance can move beyond the repair budget. It can affect insurance, owner confidence, and the corporation’s financial position for years.

What a harder insurance market means for boards

In British Columbia, strata insurance premiums rose between 50% and 400% in a single renewal cycle between 2019 and 2022, according to the BC Chamber of Commerce. Ontario did not see the same level of crisis, but boards still felt the pressure. Aging buildings, repeated water claims, and rising repair costs all pushed insurers to price risk more aggressively.

When the insurance market hardens, insurers become more selective. They raise deductibles, narrow coverage, add conditions, and may decline buildings with poor claims records. Buildings with repeated water losses usually feel it first.

In the webinar, Lyndsey McNally pointed out that the last hard market was not long ago. Premiums were rising, deductibles were climbing, and some buildings had trouble finding coverage. The market has softened since then, but soft markets do not last forever. If a corporation has a poor water claims history, the next turn in the insurance cycle can hit quickly.

A single water damage claim can also affect premiums. Research published by the Insurance Institute of Canada and reported in Canadian Underwriter found an average 19% increase after a water damage claim in a homeowner and condo-related insurance context. For a corporation with multiple water claims, the renewal conversation can become much harder.

Fast response matters. So does prevention. But boards also need to know how they would pay the corporation’s share of the loss if a major water event happened tomorrow.

How boards usually respond when the bill arrives

Over the past several years, CLG has worked with Ontario condo boards that contacted us after a significant water event. The pattern is familiar.

The leak happens. Emergency responders arrive. Restoration starts. A few weeks later, once the scope is clearer, the financial problem lands on the board table. The deductible is $150,000, maybe $200,000. The reserve fund has $60,000 available. The property manager says, “We may need a special assessment.”

That is often the first time the board hears about corporation borrowing as an option.

Special assessments are simple on paper. The board passes the required resolution, owners are billed, and the corporation collects the money. In practice, it is rarely that clean. Some owners do not have the cash. Some object. Some ask lawyers. Collection can drag on while the corporation’s invoice is already due.

There is also political fallout. A board that delivers a $15,000 special assessment may be right on the numbers and still lose owner confidence.

Borrowing is not always the answer. But it should be on the table before the board assumes a lump-sum assessment is the only path.

Understand the difference between special assessment financing and corporation borrowing. Visit our special assessment financing page.

Condo insurance deductible financing vs. a special assessment

A condo corporation loan works differently from a special assessment in one basic way: owners do not receive a separate lump-sum bill. The corporation borrows the required amount. Repayment is built into monthly common expenses over the loan term. Owners see a monthly increase rather than a five-figure invoice.

Borrowing is not right for every situation. A small deductible or a well-funded reserve may not justify a loan. But where the uninsured cost is large and available cash is limited, the comparison is worth making.

| Special assessment | Corporation loan | |

|---|---|---|

| Payment structure | Lump sum billed to each unit | Monthly common expense increase |

| Owner impact | Often thousands per unit, paid upfront | Lower immediate impact, spread over the loan term |

| Political risk | High. Owners may object, delay payment, or dispute the assessment | Usually easier to communicate than a large lump-sum assessment, but owner communication still matters |

| Collection risk | Some owners may not be able to pay right away | Collected through the common expense process, which is usually more structured |

| Timing | Can be unpredictable if collection is slow | More predictable once the loan closes |

| Ontario bylaw requirement | No borrowing bylaw required | Borrowing authority or a borrowing bylaw is required |

In Ontario, a condo corporation must have valid borrowing authority before taking on debt. That often means a borrowing bylaw. In many cases, the voting threshold is a simple majority of all unit owners, not just the owners present at the meeting. Some corporations already have borrowing provisions in their existing bylaws, especially for smaller amounts.

If the issue is an insurance deductible or a smaller prevention investment, the corporation may already have the authority it needs. For larger amounts, a specific purpose borrowing bylaw is often required. The board should not rule out borrowing before checking the governing documents and getting legal advice.

At CLG, we have supported the bylaw process in 9 out of 10 cases where we have been engaged. We provide templates, owner letters, and presentation materials so owners can understand the numbers before they vote. When owners are looking at a real financial problem, such as a large deductible, failed risers, or water damage affecting their units, they are more likely to pay attention and participate.

Ontario condo corporations may be able to borrow funds to cover water damage deductibles, emergency repairs, and self-insured losses if proper borrowing authority is in place under the Condominium Act. As of March 2025, Ontario had 13,318 registered condo corporations serving 933,751 residential units, according to the Condominium Authority of Ontario. Corporation borrowing can spread the cost through common expenses instead of relying only on a lump-sum special assessment.

Learn more about how condo corporation financing works. Visit our condo and strata financing page.

How CLG helps boards fund the gap

Condominium Lending Group lends directly to condo corporations and strata councils. The loan is not made to individual owners. When a water event creates unexpected financial pressure, CLG can help fund:

- the insurance deductible, once the loss is assessed;

- emergency repair costs, including repairs to the failed system that caused the leak;

- self-insured losses below the deductible threshold; and

- reserve fund replenishment after emergency costs draw down available cash.

CLG also provides no-cost financial plan reviews for boards that want to understand their exposure before the next water event. If the building’s plumbing is aging, the deductible doubled at renewal, or the reserve fund study does not account for water event risk, a financial review can help the board see the options before there is pressure to act.

As of March 2025, Ontario had 13,318 condo corporations managing 933,751 residential units and 1.82 million residents, according to the Condominium Authority of Ontario. Many of those corporations do not have a clear funding plan for a large water event. Some may never need one. Others will wish they had one ready.

Get in touch with our team for a no-cost financial plan review. Contact CLG to get started.

Frequently asked questions

Can a condo corporation borrow money to cover an insurance deductible?

Yes. In Ontario, a condo corporation may be able to borrow funds for a common element purpose, including an insurance deductible, if the proper borrowing authority is in place. That may require a borrowing bylaw approved by unit owners, depending on the corporation’s documents and the amount being borrowed. CLG specializes in loans to condo corporations and strata councils for these kinds of situations.

What costs from a water event does property insurance not cover?

Property insurance usually covers resulting damage, such as damaged drywall, flooring, cabinets, and finishes. It does not usually cover the cause of the loss. If a plumbing riser or pipe fitting fails, the corporation may have to pay for the repair or replacement. Insurance also does not cover the deductible or losses below the deductible threshold.

Is a special assessment the only option when the reserve fund does not cover a water damage deductible?

No. A condo corporation may be able to borrow to cover the gap, then repay the loan through monthly common expenses. Proper borrowing authority is required first, which may include a borrowing bylaw. Timing depends on the corporation, the approval path, and the required owner communication. See our frequently asked questions about condo corporation loans for more on how borrowing works.

What is a self-insured retention in condo insurance, and why does it matter?

A self-insured retention is the amount the corporation pays from its own funds. In many practical discussions, boards use it to describe losses that fall below the deductible threshold. If the building has a $100,000 deductible and a water event causes $35,000 in damage, that $35,000 is the corporation’s cost. As deductibles rise, more events fall below the threshold.

How does the insurance market affect a condo corporation’s deductible over time?

Claims history matters. A corporation with repeated water claims may face higher premiums, higher deductibles, and more restrictive coverage. In BC, strata insurance premiums rose sharply between 2019 and 2022. Ontario saw a softer version of the same pressure. Buildings that reduce claim frequency and document their response well may be in a better position at renewal.

Does borrowing to pay a water damage deductible increase condo fees?

Usually, yes. The loan is repaid through monthly common expenses, so owners may see a monthly increase. The point is that the cost is spread over time instead of billed as a large lump sum. The exact monthly impact depends on the amount borrowed, the number of units, and the repayment term. CLG can model this for the board as part of a no-cost financial plan review.

Plan before the next water event

Water events create several financial problems at once. Insurance handles some of the damage, but not all of it. The deductible, smaller self-insured losses, and repairs to the failed system can still leave the corporation with a large bill.

The boards that handle these situations best usually know three things before the event happens: the deductible, the available cash position, and whether borrowing is an option. That does not mean they borrow every time. It means they are not guessing during a crisis.

If your board is not sure about those three things, a financial review is a sensible first step. Our team can walk through the options before the next water event, not during it.

Ready to understand your options? Contact our team to book a no-cost financial plan review.

Expert contributors

- Aaron Norgaard, NorGaard Solutions, water event prevention, pipe corrosion management, and leak detection systems

- Amanda Silvestri, Renolux Restore Group, emergency water event response, moisture control, and restoration

- Lyndsey McNally, Condominium Lending Group, condo corporation financial planning and financing

- Ruth Tompkins, LEaC Shield, water event risk management

Watch the Webinar

Watch the full webinar here: Water Events: Prevention, Response and Financial Impact

Sources

- Condominium Authority of Ontario, By the Numbers: CAO Registry Data, retrieved 2026-05-27

- Insurance Bureau of Canada, 2024 Shatters Record for Costliest Year for Severe Weather-Related Losses in Canadian History at $8.5 Billion, January 2025, retrieved 2026-05-27

- TD Insurance Home via IBC, Water Damage in Condo Buildings, cited in Condo Control, retrieved 2026-05-27

- Canadian Underwriter, One Knock-Off Effect of Rising Condo Deductibles, retrieved 2026-05-27

- RCLLP Condo Law, What’s a Reasonable Deductible for Condominiums?, retrieved 2026-05-27

- Canadian Underwriter, Behind the Hard-Hit Condo Insurance Market in B.C. and Alberta, retrieved 2026-05-27

- BC Chamber of Commerce, Strata Insurance Premium Crisis 2023, retrieved 2026-05-27

- Daily Hive / BC Financial Services Authority strata insurance report data, Vancouver Strata Insurance Premiums Report, June 2020, retrieved 2026-05-27

- Hudson HVAC, Plumbing Riser Replacement, retrieved 2026-05-27

- Insurance Institute of Canada / Canadian Underwriter, How Even a Single Water Damage Claim Affects Your Homeowner Clients, 2025, retrieved 2026-05-27